If you want to build your Retirement corpus serisioly than this Retirement Planning in 30s, 40s & 50s India: A Complete Age-Wise Guide is going to definitely help you wth many tips and tricks. Basically Retirement. Planning is not a one-time activity it is a journey that changes with your age, income, and responsibilities.

The financial decisions you make in your 30s, 40s, and 50s can significantly impact the quality of your retirement life.

In India, retirement planning has become more important than ever due to rising inflation, increasing life expectancy, and lack of guaranteed pensions for most private employees.

This complete guide explains retirement planning in 30s, 40s & 50s in India, helping you understand what steps to take at each stage of life.

Table of Contents

Why Retirement Planning by Age is Important in India

Many people believe retirement planning can wait until their 40s or 50s. But delaying retirement planning increases financial pressure later in life.

In India, several factors make retirement planning essential:

- Increasing life expectancy (people living up to 80–90 years)

- Rising healthcare expenses

- Inflation reducing purchasing power

- Limited pension benefits in private jobs

- Changing family structures and financial responsibilities

Top 5 reasons Why Retirement Planning important & Why Every Indian Needs It?

Retirement Planning in Your 30s in India

Your 30s are the best time to start retirement planning because you have the biggest advantage with you i.e.time.

Even small investments made early can grow into a large retirement corpus due to the power of compounding.

Financial Situation in 30s (Typical in India)

Most individuals in their 30s:

- Start earning stable income

- Get married or start families

- Take home or personal loans

- Begin financial responsibilities

- Have growing expenses

Despite these commitments, this decade is the most powerful period for retirement planning.

Key Steps for Retirement Planning in Your 30s

1.Start Investing Early

The earlier you start, the less you need to invest later. At this stage you can invest aggressively in the following avenues:

Even investing Rs 5,000- Rs 10,000 monthly can create significant wealth over time.

SIP for Retirement – The Smart Way to Secure Your Future

How to Start SIP in India– Explained in baby steps

2.Build an Emergency Fund

Before any aggressive investing, creation of at least 6 months of expenses as emergency savings is necessary

This prevents disruption to your retirement investments during emergencies.

3.Buy Term Insurance

If you have dependents, life insurance is essential. one must have at least 15-20 times annual income worth coverage.

4 Invest More in Equity

Since retirement is far away. Equity investing can be somwhere between 70-80% of the corpus and rest 20-30% debt allocation can be followed. This helps maximize long-term returns.

Disclaimer: please consult your Financial Advisor before concluding any allocation.

5. Increase Investments Every Year

Increase SIP amounts with lumpsum payments at each salary increments or on yearly basis can further multiply your corpus.

This simple habit builds a strong retirement corpus.

Step Up SIP can make you Millionaire- Know how?

Mistakes to Avoid in Your 30s

- Delaying retirement investments

- Investing only in fixed deposits/ debt investments

- Ignoring insurance

- Spending without saving

- Not increasing SIPs regularly

Retirement Planning in Your 40s in India

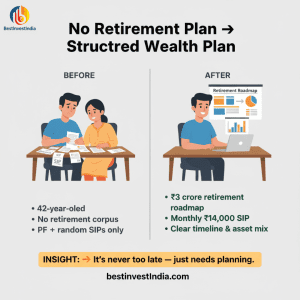

If you have not planned your investments yet and not saved for your retirement than your 40s are a crucial decade where retirement planning should become more serious and disciplined.

This stage usually brings higher income but also higher responsibilities.

Financial Situation in 40s

Most individuals in their 40s:

- Have peak earning potential

- Face children’s education expenses

- Manage home loan commitments

- Experience lifestyle inflation

- Balance multiple financial goals

Key Steps for Retirement Planning in Your 40s

1. Increase Retirement Contributions

Since you have already lost significant time of your life. Retirement Planning in Your 40s need higher investing commitment.

At this stage:

- Start with high SIP amounts

- Add Lumsum at a fixed interval

- Invest bonuses wisely

- Allocate more funds toward retirement

- Save at least 20–30% of income

2.Review Retirement Goals

Retirement Planning becomes highly crucial here, since financial mistakes at this stage may become heavy o your future financial well being. Existing investment review for your critical goals and Retirement Planning is must at this stage.

Estimate:

- Retirement age

- Monthly expenses

- Inflation-adjusted expenses

3.Balance Equity and Debt

Retirement planning for 40 year old India are requires high equity allocation somewhere between 60–70% and rest in debt investments. This ensures balanced growth and safety.

4. Avoid Withdrawal from Retirement Funds

Avoid using retirement savings for:

- Vacations

- Lifestyle upgrades

- Short-term needs

This disrupts long-term growth.

5.Review Insurance Coverage

A health coverage is a must at this stage since a long hospitalization can wipe out years of saved money.

Ensure:

- Adequate health insurance

- Updated term insurance

- Critical illness coverage

Medical costs rise significantly with age.

Mistakes to Avoid in Your 40s

- Underestimating retirement expenses

- Ignoring inflation

- Investing too conservatively

- Withdrawing long-term investments

- Ignoring health insurance

Retirement Planning in Your 50s in India

Retirement Planning in 50s in India is highly critical. Your 50s are the final preparation stage before retirement.

At this stage, wealth protection becomes more important than aggressive growth.

Financial Situation in 50s

Most individuals in their 50s:

- Approach retirement age

- Have reduced earning years left

- Face healthcare concerns

- Support family responsibilities

- Require stable income planning

This decade focuses on preserving wealth and ensuring financial readiness.

Key Steps for Retirement Planning in 50s

1.Evaluate Your Retirement Corpus

For retirement planning checklist in 50s please evaluate the following:

- How much retirement savings do I have?

- How much more do I need?

If there is a gap:

- Increase savings/investments

- Reduce expenses

- Delay retirement if required

2.Reduce Investment Risk

Since 50s are a almost approached goal time the equity allocation should be low as compared to early ages.

Suggested allocation:

- 40–50% Equity

- 50–60% Debt

Shift gradually to safer investments.

3.Eliminate Loans

If you still have loan liabilities on you try to :

- Close home loans

- Pay off personal loans

- Enter retirement debt-free

Debt reduces retirement income security.

You can book your Free 15 min financial Planning session with us.

4.Plan Retirement Income Sources

Focus on creating:

- Monthly income streams

- Stable withdrawal plans

- Tax-efficient income strategies

Possible income sources:

- SWP (Systematic Withdrawal Plan)

- Pension income

- Interest income

- Rental income

5.Prepare Healthcare Funds

Healthcare expenses increase significantly in later years. Therefore you must ensure:

- Adequate health insurance

- Medical emergency fund

Mistakes to Avoid in Your 50s

- Taking unnecessary risks

- Ignoring inflation

- Keeping money idle

- Delaying retirement planning

- Ignoring healthcare needs

Retirement Planning Comparison by Age in India

| Factor | 30s | 40s | 50s |

|---|---|---|---|

| Primary Goal | Start Early | Accelerate Savings | Protect Wealth |

| Risk Capacity | High | Moderate | Low |

| Equity Allocation | 70–80% | 60–70% | 40–50% |

| Debt Allocation | 20–30% | 30–40% | 50–60% |

| Focus | Growth | Balance | Protection |

How Much Retirement Corpus is Needed in India?

The required retirement corpus depends on:

- Current expenses

- Retirement age

- Life expectancy

- Inflation rate

For example:

If current monthly expenses are 50,000 than the estimated retirement corpus required can be between Rs 4–7 Crore

This highlights the importance of starting retirement planning early.

How much is enough for retirement in India?

Sample Retirement Planning Strategy by Age in India

Age 30

- Start Rs 10,000 SIP

- Invest in equity funds

- Begin NPS contributions

- Increase investments annually

Age 40

- Increase SIP to Rs 30,000+

- Review retirement corpus

- Balance equity and debt

- Strengthen insurance

Age 50

- Shift to safer investments

- Build retirement income strategy

- Reduce liabilities

- Prepare withdrawal plan

Start SIP from our investment platform

https://bestinvest.themfbox.com/

Final Thoughts: Retirement Planning in 30s, 40s & 50s India

Retirement planning is not about how much you earn—it is about how early and consistently you invest.

No matter your age today, the best time to start retirement planning is now.The earlier you begin, the easier it becomes to build a secure and comfortable retirement life.