How to create a financial plan in India is one of the most important questions every salaried individual and family should ask. Many people earn well, save regularly, and invest occasionally, yet still feel financially stressed or uncertain about their future. The reason is simple – income alone does not build wealth, planning does.

A personal financial plan acts like a roadmap. It tells you where you are today, where you want to go, and how to reach your financial goals without confusion or costly mistakes.

In this article, you will learn a simple step-by-step method to create your personal financial plan in India.

Table of Contents

Step-by-Step Financial Planning for Beginners in India

To start Financial Planning for Salaried Employees in India, you need to follow below mentioned steps. You might have covered few steps but this Complete Guide to Financial Planning in India will definitely help you with Personal Financial Planning.

Step 1: Understand Your Current Financial Situation

Before planning your future, you must clearly understand your present financial condition.

Most people avoid this step because they feel uncomfortable looking at numbers. However, this is the foundation of financial planning.

You can start by listing:

- Your income

- Monthly Expenses

- Loans and EMIs

- Savings and Investments

- Insurance policies

- Health Insurance

- Accidental insurance

- Critical care Insurance

Create a simple summary of:

- Monthly income from salary or business

- Monthly household expenses

- Outstanding loans such as home loan, car loan, or personal loan

- Existing investments such as mutual funds, fixed deposits, provident fund, or stocks

- Insurance coverage such as life insurance and health insurance

This step helps you identify where your money is going and whether you are financially stable.

Step 2: Set Clear Financial Goals

Financial planning without goals is like travelling without a destination. You must define what you want to achieve financially.

Financial goals generally fall into three categories:

1.Short-term goals

These are goals within 1 to 3 years. Examples include building an emergency fund, buying a vehicle, or planning a vacation

2.Medium-term goals

These are goals within 3 to 7 years

Examples include buying a house, starting a business, or funding children’s education or other goals.

3.Long-term goals

These are goals beyond 7 years

Examples include retirement planning, wealth creation, and children’s higher education

Make sure your goals are specific and realistic. For example: Instead of saying save for retirement ,Say build a retirement fund of 2 crore in 20 years

Clear goals make planning easier and measurable.

How to set Financial Goals SMARTLY

Step 3: Create a Monthly Budget

Budgeting is one of the most powerful tools in personal finance. Without budgeting, even high earners struggle financially.

Divide your expenses into categories:

Essential expenses

- Rent or home loan

- Groceries

- Utilities

- School fees

- Insurance premiums

Lifestyle expenses

- Dining out

- Shopping

- Entertainment

- Travel

Savings and investments

A simple rule many people follow is:

Needs– 50 percent for essential expenses

Wants– 30 percent for lifestyle expenses

savings -20 percent for savings and investments

If your savings rate is lower than 20 percent, it is time to adjust your spending.

Budgeting ensures that you save consistently and avoid unnecessary financial stress.

Salary Comes But No Savings? Here’s How to Save More Every Month

Step 4: Build an Emergency Fund

An emergency fund protects you during unexpected situations.

Emergency may include:

- Job loss

- Medical emergencies

- Business losses

- Urgent repairs

Ideally, your emergency fund should cover:

Six months of household expenses for salaried individuals

Nine to twelve months of expenses for business owners

Keep your emergency fund in:

- Savings account

- Liquid mutual funds

- Short-term fixed deposits

Do not invest this money in risky investments such as stocks. An emergency fund prevents you from taking loans during difficult times.

Emergency Fund Guide : Emergency Fund Investment: Why do you need it?

Step 5: Get Adequate Insurance Coverage

Insurance is often ignored, yet it is one of the most critical parts of financial planning.

Without proper insurance, one medical emergency or accident can destroy years of savings.

The basic insurance coverage every family in India should have includes:

Health insurance

It protects you from rising medical expenses.

How to decide health insurance cover amount?

Term life insurance

It protects your family financially in case of your absence.

What is Term insurance-Advantages & Details

Personal accident insurance

It covers disability and accidental risks

Pro Tip

Avoid buying insurance only for tax saving purposes. Choose coverage based on actual financial needs.

Insurance protects your financial plan from unexpected risks.

Step 6: Manage and Reduce Debt

Loans are common, but excessive debt can destroy financial stability.

Start by listing:

All outstanding loans, Interest rates, EMI amounts & Loan tenure. Start by Focussing on paying high-interest loans first, such as: Credit card dues and Personal loans

Home loans and education loans are generally considered manageable if planned well. Reducing debt improves your monthly cash flow and increases your savings capacity.

Step 7: Start Investing for Your Goals

Saving money alone is not enough to build wealth. You must invest to grow your money.

Investment options available in India include:

- Mutual funds

- Fixed deposits

- Public Provident Fund

- Employees Provident Fund

- National Pension System

- Stocks

- Bonds

Choose investments based on:

- Your goals

- Your time horizon

- Your risk tolerance

For example:

Short-term goals may require safer investments

Long-term goals benefit from growth-oriented investments like equity mutual funds

Regular investing through systematic plans helps create wealth over time.

Financial Goal Planning in India: A Practical Guide with Examples

How to start investing Today: A Beginner’s Guide to Growing Wealth

Step 8: Plan for Retirement Early

Retirement planning is often delayed, but starting early makes a huge difference.

Many people assume pension or provident fund will be enough, but rising costs make retirement expensive.

Estimate:

- Your expected retirement age

- Monthly expenses after retirement

- Inflation impact

- Life expectancy

Start investing in retirement-focused instruments such as:

- Employees Provident Fund

- Public Provident Fund

- National Pension System

- Mutual funds

Early retirement planning reduces financial pressure later in life.

Retirement Planning in 30s, 40s & 50s India: A Complete Age-Wise Guide

9 Super Easy Steps to Retirement Planning

Step 9: Save Taxes Legally and Efficiently

Tax planning is an important part of financial planning in India.Use tax-saving instruments such as:

- Section 80C investments

- Public Provident Fund

- Employees Provident Fund

- Equity Linked Saving Scheme

- Life insurance premiums

Health insurance premiums qualify under Section 80D. Proper tax planning helps you save money and increase overall returns.

Avoid investing only for tax saving. Always align tax saving with financial goals.

Step 10: Review and Update Your Financial Plan Regularly

Financial planning is not a one-time activity. Life changes, and your financial plan must change with it.

Review your plan:

- Once every year

- After major life events such as marriage, childbirth, or job change

- When income increases

Check whether:

- You are meeting your financial goals

- Your investments are performing well

- Your insurance coverage is adequate

Regular reviews keep your financial plan effective and relevant.

Common Mistakes to Avoid While Creating a Financial Plan

Many people struggle because of avoidable mistakes.

Some common mistakes include:

- Investing without clear goals

- Ignoring insurance needs

- Taking excessive loans

- Not building an emergency fund

- Delaying retirement planning

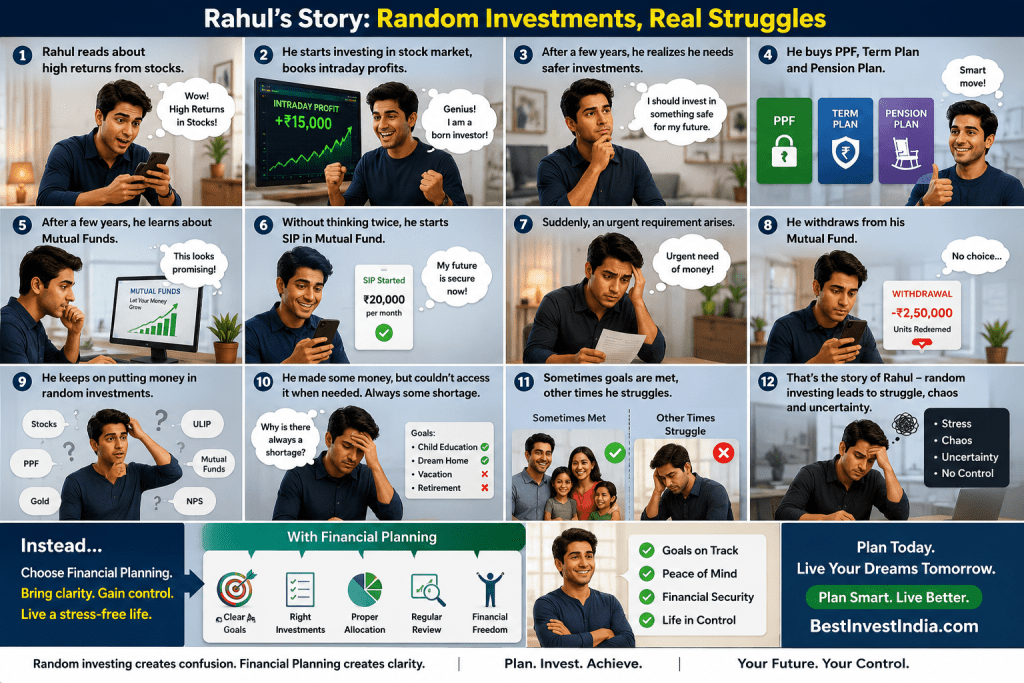

- Following random investment advice

Avoiding these mistakes can save years of financial stress.

11 Financial Mistakes Indians Make in Their 30s and 40s (And How to Avoid Them)

Benefits of Creating a Personal Financial Plan

A proper financial plan provides several long-term benefits.

These include:

- Better control over money

- Reduced financial stress

- Clear direction toward goals

- Improved savings discipline

- Protection against financial risks

- Faster wealth creation

- Peace of mind for family

Financial planning turns uncertainty into clarity.

When Should You Seek Professional Financial Help

Many individuals try to manage finances on their own but feel confused due to multiple options and changing financial products.

You should consider professional help if:

- You are unsure how to start investing

- You have multiple financial goals

- You want to reduce financial mistakes

- You are planning retirement

- You want a structured investment strategy

- You feel financially stressed despite earning well

Professional guidance ensures your financial decisions are aligned with your goals.

Discover 10 reasons: Why Financial Advisor for Common People is needed?

Final Thoughts

Creating a personal financial plan in India is not just about managing money. It is about building a secure future for yourself and your family.

The earlier you start, the more time your money gets to grow. Even small steps taken today can create meaningful financial security tomorrow.

Financial planning is not only for wealthy individuals. It is essential for common people, salaried employees, and families who want stability, growth, and peace of mind.

Start today, review regularly, and stay committed to your financial journey.

{kind=link}